Fashion’s multi-brand retailers are under pressure with Canadian e-tailer Ssense the latest to feel the heat.

Last month, the ailing Gen-Z favourite, once valued at more than $4 billion, said it was filing for bankruptcy protection, citing mounting debt amid changes to US trade policy, after creditors pushed for a sale. The news came just two weeks after Florence-based LuisaViaRoma also filed for court protection from creditors.

If the collapse of Barneys New York in 2019 was a warning sign that all was far from well in multi-brand retail, the dominoes have kept falling. Last year, London-based e-tailer MatchesFashion shut down, while sprawling Farfetch, a Wall Street darling at its peak, was narrowly saved from collapse by South Korean e-commerce giant Coupang, which has stabilized the platform but turned it into a de facto grey market seller, forced to find stealthy workarounds to continue to offer top brands that defected after the sale.

Then, earlier this year, US luxury department store giant Saks found itself unable to pay brands and was forced to refinance its $2.2 billion bond, which analysts saw as, effectively, a default.

The turmoil has caused upheaval in the market for luxury fashion, where consumers prefer to shop across brands and many independent labels depend on third-party retailers for distribution.

Multi-Brand in Crisis

In recent years, major luxury brands have invested heavily in steering customers to their own stores and websites, which offer higher profit margins and greater control over the shopping experience, and sharply reduced their exposure to wholesale, contributing to the channel’s near collapse.

This has put added pressure on e-tailers, already struggling with high customer acquisition costs, and department stores, long suffering from changing consumer habits.

But e-tailers and department stores have also been bruised by their own strategies as they prioritised scale over customer service and curation, diluting their raison d’etre. While key e-tailers emphasised traffic over a unique experience, becoming indistinguishable from one another, many major department stores expanded aggressively into new markets, cutting staff and service levels to manage costs.

“If you have companies headquartered in New York or Dallas, you have people trying to manage the experience in markets they don’t like or travel to very often,” said Molly Nutter, president of ByGeorge who served as a merchant for Barneys for two decades. “It becomes an uphill battle to create something special.”

A Blank Space

The decline of multi-brand retailers has created a fundamental dilemma for small and medium-sized fashion brands, which can’t typically generate sufficient sales per square foot or drive enough traffic to their websites to make direct sales a viable strategy and therefore remain dependent on third-party retailers.

“New generation small brands have embraced brand.com digital distribution, but serendipitous encounters between brands and consumers are challenged in this model, limiting success to volatile and ultimately unsustainable ‘winner-takes-all’ booms and busts,” said Bernstein analyst Luca Solca.

At the same time, shoppers continue to crave the discovery and curation that only multi-brand environments can provide. Shopping behaviour studies show that customers still prefer browsing across multiple brands in a single session, whether online or in-store, rather than visiting individual brand websites or boutiques.

“Customers do want experiential moments — they want to go into a store and see someone they know and be a part of a community,” said Amy Williams, chief executive of denim label Citizens of Humanity.

Making Multi-Brand Work

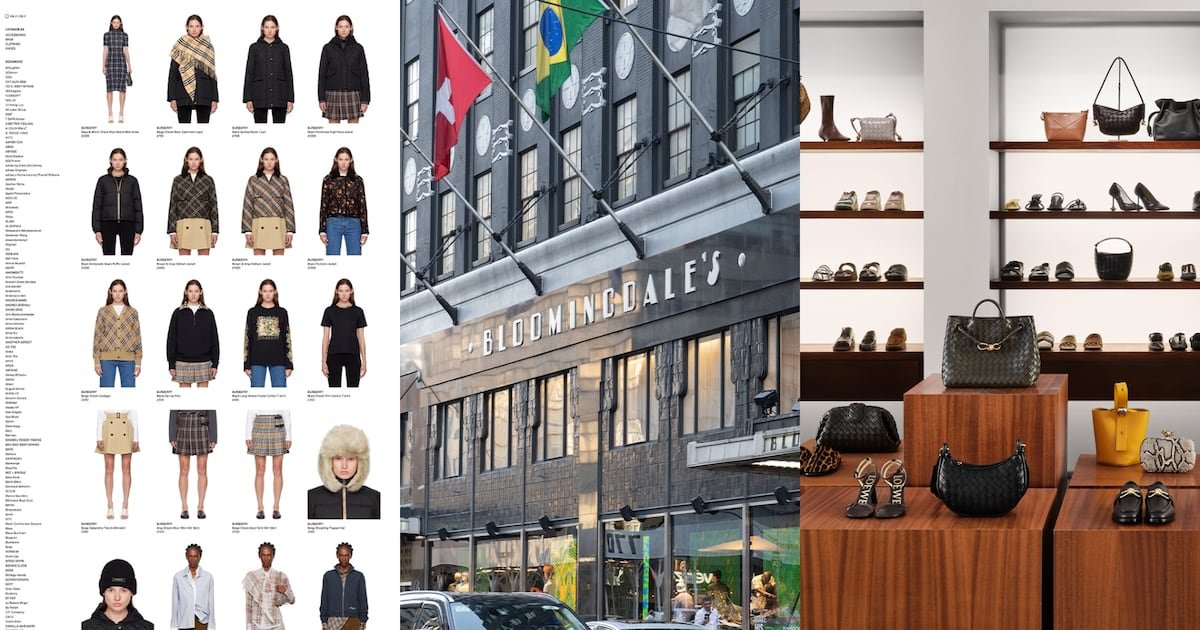

Bloomingdale’s is an unlikely success story, proving that the department store model isn’t inherently broken — it requires financial discipline, investment in brand partnership and prioritising customer service. In recent months, it has begun store renovations across its footprint and boosted the headcount of its sales associates. The Macy’s Inc.-owned retailer saw sales increase 4.6 percent in its most recent quarter.

“We’re ready to invest,” said Bloomingdale’s chief executive Olivier Bron. “Our biggest source of inspiration are local specialty retailers. They are very focused and are obsessed about their customer.”

Indeed, independent specialty retailers such as ByGeorge in Austin, Texas, Hirshleifers in Long Island, New York, McMullen in San Francisco, Dover Street Market and more are a bright spot amid the turmoil.

In 2024, independent boutiques drove 59 percent of transaction volume on wholesale software platform Joor, up from 47 percent in 2019, said Amanda McCormick Bacal, the company’s global head of marketing.

Shoppers gravitate toward their intimate, curated environments where discovery feels personal, rather than mass and transactional. These boutiques also move with agility — quickly adapting their buys and spotlighting emerging designers. At ByGeorge, the sales floor is reset at least once every two weeks, according to Nutter.

“Where you’re seeing the specialty stores winning market share is they’re very thoughtful about their investments,” Bacal said. “They really have a clear picture of who their clientele is, they tend to have excellent in-store presentations and very well-trained and knowledgeable staff.”

Leading luxury e-tailers like Mytheresa bank on targeting top-spenders, thereby getting a better return on customer acquisition costs. But they also lean heavily into tight curation and customer service. Online womenswear retailer Cult Mia, which sells ornate eventwear from contemporary luxury labels, only onboards around 10 percent of the 250 brands that seek to join the platform each month, said founder Nina Briance.

Some successful e-tailers are also investing in new technology to enhance product discovery. Garmentory, which provides a platform for independent boutiques, is launching an AI search tool in the fall that generates results from specific prompts, taking into account that “people don’t want to search for a checkered shirt or a black dress; they want to shop based on how they plan to use it,” said Sunil Gowda, founder and chief executive of Garmentory, which is on track for 25 percent year-over-year sales growth 2025.

“The best models are balancing efficiency with serendipity,” Bacal said. “The best models help customers find what they’re looking for quickly but also stumble upon something that maybe they didn’t know that they needed. The balance between those two things creates the most effective product discovery.”

What Lies Ahead

As specialty retail continues to gain market share, the answer for US department store giants may be downsizing. “Maybe the answer is, ‘We don’t need 40 stores, but 20 stores and our staff has to be well-trained,’” said Marigay McGee, a former top executive at Saks Fifth Avenue and Harrods.

After merging with Neiman Marcus last year, Saks Global, for instance, has closed several locations to minimise cannibalisation. Macy’s, too, will have culled half of its total footprint by the end of next year.

Successful stores today are run like hotels, according to McGee, where customers are the guests and sales associates behave like concierges. “They have to invite people in to experience their brands, and make sure their stay is as amicable as possible,” she said, pointing to new necessary amenities like cafés, seating areas and beautiful bathrooms. “The point is for people to want to stay and spend time.”

At the same time, major retailers have a scale advantage that affords them the kind of marketing muscle no independent boutique could dream of. “The visibility, the audience — we have the ability to simply invest more than the specialty stores, so we can be more sophisticated in our relationship with brands,” said Bron.

Bloomingdale’s has boosted its brand partnerships by investing in branded marketing such as pop-ups and brand-specific in-store activations, as well as integrating more small emerging labels into its brand matrix, such as London-based Liberowe and Greek jewellery designer Ileana Makri.

Still, the irony is that the future of multi-brand retail may look a lot like its past.

Boutiques that offer genuine discovery and service — qualities that, along with convenience, the best department stores once delivered — may be poised to seize further market share.

Large department stores and e-tailers have become “supermarkets of fashion,” said fashion commentator and StyleZeitgeist editor Eugene Rabkin. “Specialty stores are the ones who may actually be in a better place because they have retained what consumers like: a point-of-view, a direction, which cultivates loyalty.”

Read “The Great Fashion Reset,” a special package on the challenges facing fashion and the way forward, as the industry enters a historic, high-stakes season.