After several years of post-pandemic reset, the hospitality and leisure dealmaking sector is settling into a new rhythm. Growth is no longer about adding scale alone, but about how well companies can connect experiences, customer data and loyalty across their portfolios. The assets attracting the most interest are those designed to work together.

PwC US Deals 2026 outlook for hospitality and leisure shows that deal activity held steady through 2025, even as buyers became more selective. Year-to-date deal volume was only slightly lower than last year, but the average deal was much smaller, pointing to a more disciplined market. With capital still expensive, buyers are prioritizing deals with a clear and credible path to value after closing.

That shift has favored strategic buyers. Corporates led most hospitality and leisure transactions in 2025, while private equity’s share of disclosed deal value fell to about 35%, down from nearly 60% the year prior. Corporate buyers are stepping in where private equity is pulling back, prioritizing assets that help strengthen existing ecosystems and accelerate long-term value creation.

Why connected experiences matter

One clear takeaway from recent deal activity is that standalone assets are losing ground to more integrated businesses. Buyers are increasingly focused on assets that strengthen loyalty programs, improve personalization or connect more directly with customers across channels. That helps explain why luxury resorts, digital gaming platforms and experience-led brands continue to attract interest, while other parts of the market are still catching up.

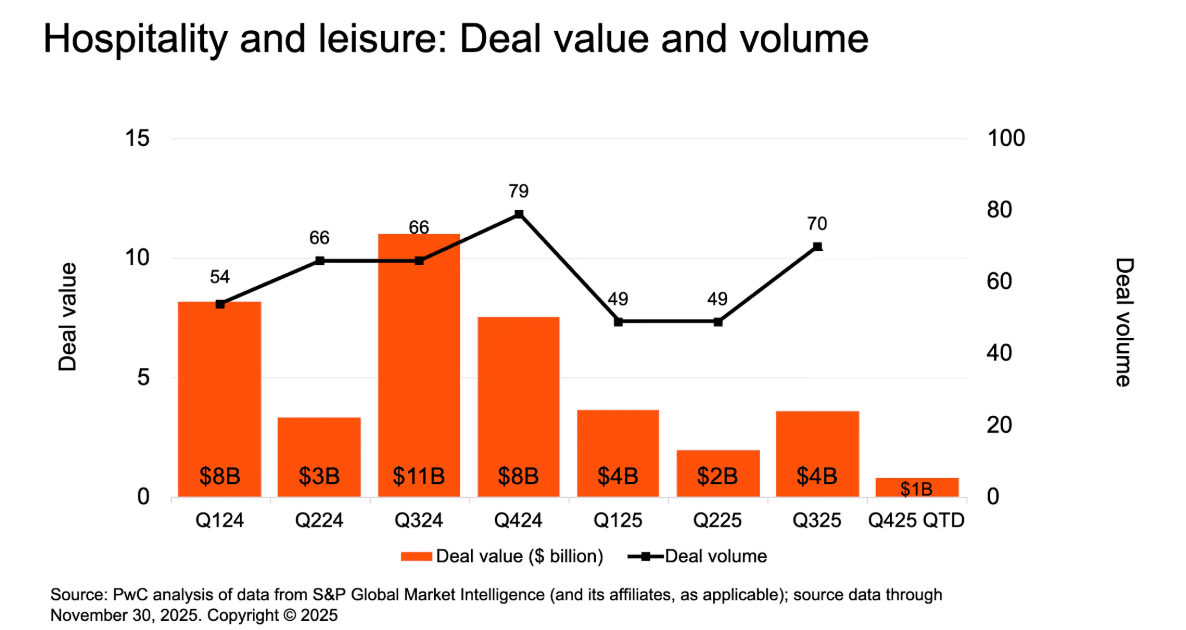

Premium experiences are holding up well. Younger and higher-income consumers continue to prioritize leisure spending, even as broader consumer caution persists. In fact, deal volume in the third quarter of 2025 jumped about 60% from the second quarter as financing conditions improved and uncertainty around trade and the broader economy eased.

Looking ahead, businesses built around connected experiences are likely to pull ahead, while businesses without strong digital and loyalty programs may find it harder to attract buyers willing to pay a premium.

AI and data move to the center of deal value

AI is already changing hospitality and leisure, but the focus is shifting. Early investments centered on guest-facing tools like digital concierges and pricing systems. Today, buyers are paying just as much attention to how AI helps run the business day to day.

That shift is reflected in where companies are investing. Back-office modernization is accelerating, with operators upgrading finance, HR, logistics and event systems to improve efficiency and support growth. These capabilities are increasingly part of the investment case, not just operational improvements.

AI is also quickly becoming a basic requirement. Companies with clean, well-organized data are better positioned to use AI in ways that can improve margins and service. Those without that foundation may struggle to keep up.

As AI use expands, data quality is emerging as a real constraint. Fragmented customer records and disconnected loyalty systems continue to limit personalization and consistency across brands.

Dealmakers are responding. There’s a growing emphasis on unified customer data and loyalty integration during diligence and post-close planning. Businesses with clear plans to bring customer data together and use it responsibly are more likely to deliver results after a deal closes.

Private equity stays selective

Private equity activity has cooled, largely due to tighter return expectations. The asset-heavy nature of hospitality and leisure adds another layer of complexity, particularly outside the luxury segment.

Even so, private equity has not stepped away. Instead, they’re focusing on deals where operational improvement, digital integration and experience-led growth can meaningfully change performance. Luxury resorts and differentiated platforms with pricing power remain key areas of interest.

Gaming continues to draw attention

Gaming has been one of the busiest areas in hospitality and leisure. In fact, the sector’s three largest deals in the second half of 2025 all involved digital gaming assets and overseas buyers. For investors, gaming stands out because it can combine digital scale with repeat, data-driven engagement.

As entertainment, technology and hospitality continue to overlap, gaming platforms are increasingly seen as a core part of the overall experience, not just standalone businesses.

What this means going forward

Improving capital markets and steady travel demand should help bring deal activity back to hospitality and leisure. But success will depend less on doing more deals and more on choosing the right ones.

The stronger outcomes are likely to come from deals that combine strong brands with a disciplined use of data, AI-enabled operations and integrated loyalty programs. Buyers that focus early on integration, especially around data and customer engagement, can lead the way in delivering value over time.

Hospitality and leisure are no longer just about places to stay or play. They are about how well those experiences can work together. The coming year will likely show which organizations are ready to make that shif

.